Litigation Finance

Fixed-return loan notes funding claims with Supreme Court precedent — boring by design.

Fixed-return loan notes that fund firms processing high volumes of consumer-redress claims whose legal principle is already settled by the Supreme Court. No case-by-case speculation — the merits are decided, so the work is execution. Indicative returns of 12–17% per annum.

Most litigation finance is speculative: a funder backs a case, takes a share of the damages if it wins, and loses its capital if it doesn't. That is not what we present here. We are deliberately boring — and in litigation, boring is good.

We only feature opportunities that fund claim types whose legal principle has already been decided by the Supreme Court. The question of whether the claim is good law has been answered. What remains is execution: processing large volumes of qualifying claims accurately and efficiently. If a claim type doesn't have Supreme Court precedent, we don't present a product around it — it is as simple as that.

We back precedent, not speculation

Speculation on whether a novel legal argument will succeed is not our game. The firms we are comfortable with run established, precedent-backed claim types with a real track record — for example claims involving undisclosed commission (the Plevin line of cases), irresponsible or unaffordable lending, unfair credit relationships under the Consumer Credit Act, and energy mis-selling claims.

Because the underlying legal principle has already been settled by the highest court, the binary "will we win the point of law" risk that defines traditional litigation funding is largely removed before a single note is issued.

It's about processing, not potential

Once the legal merits are settled, performance comes down to operational execution: can the firm identify, onboard and process qualifying claims at volume, to a consistent standard? That is an operational question, not a speculative one. If the claims didn't have potential, they wouldn't be run — so the discipline is in the processing.

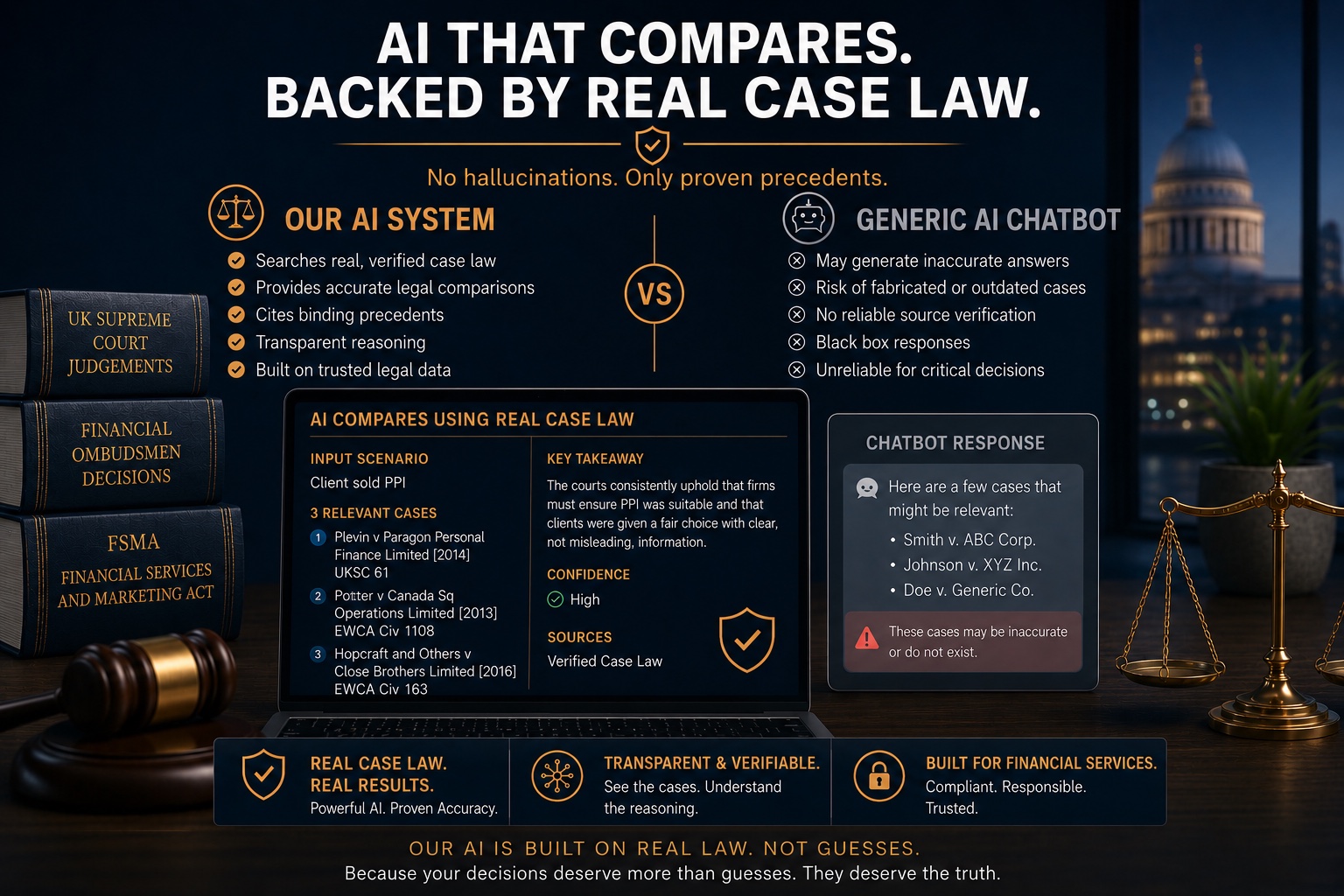

The firms we work with demonstrate exactly that — high-volume claim processing matched to strict eligibility criteria, supported by proper systems. In particular, we favour firms that use our own AI legal software: a model built to read from actual court and case data rather than generating it, so it does not fabricate or hallucinate case law. When you are processing claims at scale, a system that cites only real, verifiable authority is not a nicety — it is the difference between a clean book and an unmanageable one.

A fixed return, on a loan note

Investors are offered a fixed return on a loan note basis — not a percentage of damages and not a multiple of capital. Interest is payable on the note in 12-month cycles.

Returns have been offered in the region of 12% to 17% per annum, depending on the amount invested and the terms of the particular note. These figures are indicative of the structures we have seen and are not a guarantee of any specific return.

Why it sits outside the markets

The performance of a precedent-backed claims book depends on settled law and processing throughput, not on equity prices, interest rates or inflation. A stock-market sell-off does not change a Supreme Court precedent or stop qualifying claims being processed.

That is what makes the return profile largely uncorrelated to a traditional portfolio of shares and bonds.

How the risk is controlled

If the claim type doesn't have binding Supreme Court precedent, no product is presented. The legal merits are settled before any note is issued.

We back firms that can demonstrably run large volumes of qualifying claims to a consistent standard — execution, not experimentation.

We favour firms running our own AI legal software — a model built to read from real court and case data, so it does not fabricate or hallucinate case law.

Every defendant is checked for the ability to actually pay the claimant — a judgment is only worth what can be collected.

Claims are backed by After-the-Event insurance, in place to protect against adverse costs and downside, substantially mitigating the risk to capital.

How we assess a litigation opportunity

Every opportunity here has been through our due-diligence process, assisted by AI. For litigation finance we will only present a loan note where:

- ✓The claim type has binding Supreme Court precedent and an established track record.

- ✓The issuing firm can demonstrate genuine high-volume claim-processing capability.

- ✓Proper systems support the claims process — ideally our own AI legal software, which works from real court data and does not invent case law.

- ✓Defendants have been checked for their ability to pay the claimant.

- ✓After-the-Event insurance is in place to protect against adverse costs and downside.

- ✓The loan note terms, fixed interest rate and 12-month payment cycle are clear and documented.

- ✓The firm's eligibility criteria are strict and consistently applied.

The risks that still matter

This is a more conservative model than speculative case funding, but loan notes remain high-risk investments. The risks that matter here include:

Your return and your capital depend on the firm that issues the loan note remaining solvent and able to meet its obligations.

After-the-Event cover only protects you if the insurer pays out; policies have terms, limits and exclusions, and the insurer must itself remain solvent.

Returns depend on the firm processing qualifying claims at volume and to standard; operational failure can affect performance even where the law is settled.

Even with ability-to-pay checks, a defendant can later become unable to satisfy claims.

Loan notes are illiquid. Expect to hold for the full term; there is no reliable secondary market.

Changes in law, regulation or court procedure can affect even established claim types and the economics of the book.

Indicative rates reflect structures we have seen; the actual return on any note is set by its own terms and is not assured.

How this is regulated

These are unlisted loan notes. Litigation finance itself is not an activity regulated by the Financial Conduct Authority, and an investment in a loan note of this kind is a high-risk investment that is unlikely to be covered by the Financial Services Compensation Scheme or the Financial Ombudsman Service.

Nothing on this platform is investment advice or a personal recommendation. You should read the specific loan note's documentation in full and take your own independent financial, tax and legal advice before investing. You would contract and deal directly with the issuing firm — we do not take or hold your money.

Frequently asked questions

The traditional model is. Ours is deliberately not: we only present claim types whose legal principle is already settled by the Supreme Court, so the work is processing established claims rather than gambling on an untested legal argument.

Through a fixed return on a loan note, with interest payable in 12-month cycles — not as a share of any damages.

Indicatively in the region of 12% to 17% per annum, depending on the amount invested and the note's terms. That is illustrative of structures we have seen, not a guarantee.

Strict eligibility (Supreme Court precedent only), defendant ability-to-pay checks and After-the-Event insurance are all designed to reduce the risk to capital. They mitigate risk but do not remove it — loan notes remain high-risk and your capital is still at risk.

No. This platform is information only. You would deal and contract directly with the issuing firm's own team.

Interested in litigation finance?

Register your interest and we’ll let you know when an opportunity in this category passes due diligence. We do not take or hold your money on this platform — you would deal directly with the opportunity’s own investment team.

Register your interestNothing on this page is investment advice or a personal recommendation. Alternative investments are high-risk and illiquid; you could lose all the money you invest. Past performance is not a guide to future returns.